Unpublished May Essays Pt. 11

Unpublished May Essays Pt. 11

How the ANC is making food unaffordable

Back in May, I worked for a now-defunct Taxpayers’ Union organisation for two weeks. I wrote several articles for them which were never published. I feel they are still relevant today, and hope you find them interesting.

The South African Reserve Bank has long since had a policy of targeting 4.5% annual inflation. For much of the rich world, this would be eyewatering. But for the heavily indebted government of South Africa, keeping interest rates low and slowly printing money is a way to ease the national debt. Trouble is, that with every Rand that is minted, each rand in circulation is reduced in value; a form of stealth taxation of all citizens simultaneously.

This further favours financial institutions and public suppliers, because of an economic phenomenon called the Cantillion effect. The Cantillion effect is when money is printed or created through ease of credit, the first financial entities who receive the newly created currency receive the full value of the currency, and as each successive pair of hands receives that currency, it is devalued, as it moves through the economy increasing the total currency pool in circulation and reducing market value.

While inflation is felt most acutely by the poor, it is not always obvious to those who live and die by the newspaper headlines. After all, the Rand has been trading relatively stably against the dollar this past year, which makes imports cheaper. But the reality is that high inflation continues unabated, and the price of materials and labour will be significantly affected.

The appearance of a strong Rand is only due to the fact that the United States has been printing dollars at a historically unprecedented rate. This means that the Rand is simply inflating at the roughly same rate as the dollar. The difference is that the dollar is the world’s reserve currency, meaning that the dollars printed by the Federal Reserve devalue the dollar reserves of every nation in the world and repatriate their value to American companies, whereas the Rand’s devaluation is being used to service massive foreign debt and local debt accrued from corruption and patronage.

Cost-price inflation is not only driven by easy credit and money printing. It is also driven by market trends and structural problems in the economy. For instance, the multiple taxes imposed at the various points in the value chain, through levies, VAT, company tax, property tax, fuel tax and import duties drive market prices up. The minimum wage drives prices up too, as does strike action by unions, and the reduction in efficiency

An American Department of Agriculture (USDA) report on the state of South Africa’s cost-price inflation on basic foodstuffs demonstrates that for seven of the past ten years, inflation has been at or above the upper-limit of the Reserve Bank’s acceptable limits.

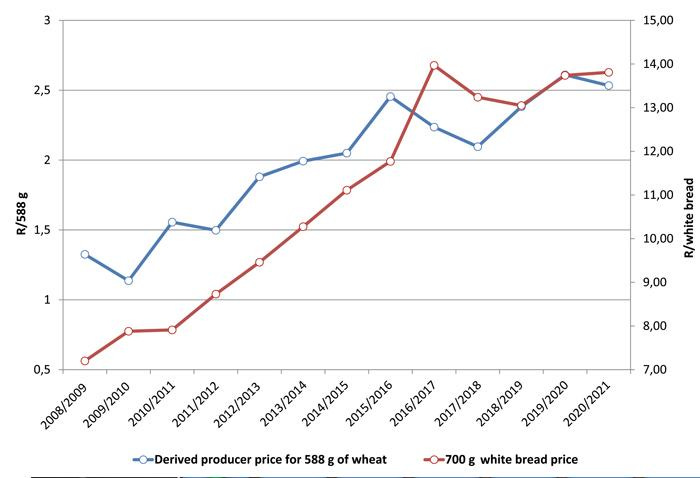

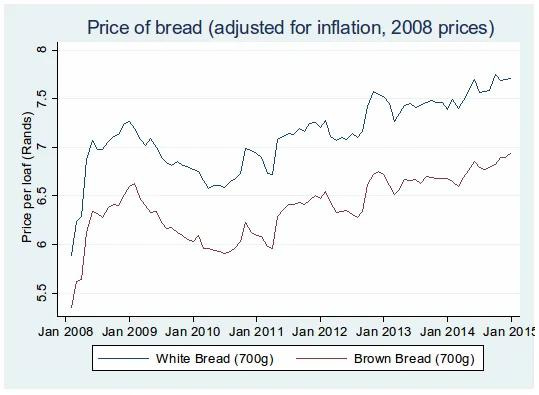

The consequences have been rapidly escalating prices of vital necessities like bread, milk and mielie pap, with bread rising from R4.68 in 2010 to R10.49 in 2015 and R14 today. This is a more rapid increase than the officially measured rate of inflation:

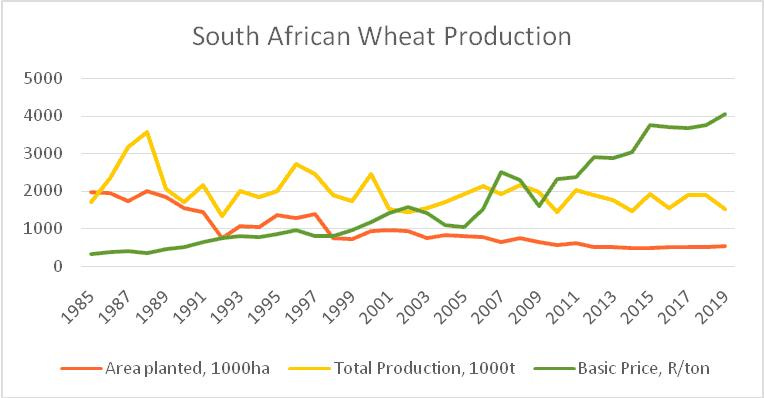

On top of this, the government plans an additional R300/ton import tarriff increase, in order to protect local markets from being swamped by lower international prices. But the necessity for such measures demonstrates the insecurity of our local farming industry, which is shrinking in terms of land area (orange) while attempting to attain the same output (yellow), resulting in climbing prices (green).

Source: Department of Agriculture, Land Reform & Rural Development

As the state puts increasing pressure on farmers through minimum wage increases, tarriffs on petrol and other taxes, and neglects their safety in terms of farm attacks, the number of farmers in the country has been on a steady decline, from 57 980 farming units in 1993 to 40 122 in 2017, a decline of 31%.Improvements in capital intensity (the amount of mechanised technology used to replace labour) has helped ease the pressure, intensive farming introduces other risks, like the effects of industrial fertilisers, pesticides and herbicides degrade soil fertility.

While total cultivated land is fairly static, SA farms have been slowly gearing away from the high-risk, low-profit-margin cash crops of staple foodstuffs toward higher-value export foods. This is due to the costs of obtaining financing, which have been increasing as drought, lawlessness and land reform have threatened agricultural land security. Their land is simply not good enough for collateral anymore.

Bread may show signs of inflation, but other food prices have leapt up due to international market pressures. The worst is cooking oil, which has jumped a whopping 13.4% in the past year,

followed by confectionary (7.4 percent), milk, eggs and cheese (7.2 percent), meat (6.7 percent) and cereals (4.9 percent) […] The substantial increase in the global price of oils and fats is due to strong demand, particularly from China, which is rapidly rebuilding its pig herd which had been reduced by the African Swine Fever. Strong global maize prices have also been driven by firm import demand from China. (see table 9 of this report)

What we see overall is a long term trend that cannot be reversed without a drastic change in the behaviour of the entire political class and a total transformation of the way of doing business. Rising prices internationally mean that many items are unavoidably increasing in price. But constant increases in taxation and fuel levies, BEE deadweight, high costs of labour, corruption, lawlessness and land reform all conspire to hobble the annual financing of staple foodstuffs by depreciating the value of the land used for collateral.

The high rate of financially driven inflation adds an extra source of pain. As the Rand becomes devalued, the last to receive new money are hit hardest. As a result, increasing economic inequality and the rise in real prices are compounded by the loss of purchasing power among the poor majority. The middle class will see their margins grow thinner each passing day, as an ever-greater share of the economy is siphoned into leaky government coffers and evaporated by the heat of the Reserve Bank’s inflation targets.